Despite Uncertainty Over Drive To Repeal Obamacare, Investors Banking On Demographics To Maintain Healthy Outlook For Health-Care Properties

Health-care REIT stocks definitely caught a cold in the wake of the unexpected November election results. Even as the Dow Jones Industrial Average topped 20,000 for the first time, the health care REIT sector has declined 2.7% over the past three months, with shares of leading companies like HCP, Inc. (NYSE:HCP) tumbling over 10% in the run up and weeks following the election.

To be sure, many market analysts acknowledge health-care markets face many unknowns, chiefly regarding any replacement for the Affordable Care Act (ACA) targeted for repeal by Republicans, and the effects of changes in government reimbursement of medical and seniors housing costs to providers.

According to a new report by the Congressional Budget Office, repealing portions of the ACA, also known as Obamacare, would cause 18 million people to lose their insurance during the first year of a new plan, and lead to 32 million more people becoming uninsured by 2026. Repeal would also lead to a doubling in the prices of premiums paid by those who remain covered in the individual insurance market, according to the CBO.

Not surprisingly, many health-care providers are expected to delay making major commitments until more information about impending changes to the Act becomes available, according to CBRE Group, Inc.’s 2017 Medical Office Building sector outlook.

While any repeal of the ACA without a replacement plan in place could bring a steep drop in health-care visits and demand, CBRE Americas Head of Research Spencer G. Levy, chief economist Jeffrey Havsy and senior managing economist Timothy Savage recently authored a report saying the long-term prospects of heath-care real estate will be affected more by the tens of millions of retiring baby boomers and ongoing health-care industry consolidation and technological advances, than by the vagaries of government health care policy.

“We are certainly in the midst of intense change and corresponding uncertainty in the health care world, particularly when it comes to government reform,” added Matthew Stevens, senior director with The Advisory Board, in a recent conversation with Colliers International Healthcare Services National Director Mary Beth Kuzmanovich. “The true keys to success are less dependent on political particularities. Providing accessible, reliable and affordable health care will remain top priorities,” Stevens said.

CBRE’s analysts also said a full repeal is highly improbable due to the negative impact of millions of Americans immediately losing their insurance and the potential for higher federal deficit spending if the tax revenue underpinning the law is not replaced. But they believe any short-term disruption will be trumped by major population trends.

“Over the long term, the wave of aging baby boomers will drive demand for health care services, irrespective of any regulatory changes,” the report said.

Outlook for MOBs Remains Solid

Health-care REIT stocks definitely caught a cold in the wake of the unexpected November election results. Even as the Dow Jones Industrial Average topped 20,000 for the first time, the health care REIT sector has declined 2.7% over the past three months, with shares of leading companies like HCP, Inc. (NYSE:HCP) tumbling over 10% in the run up and weeks following the election.

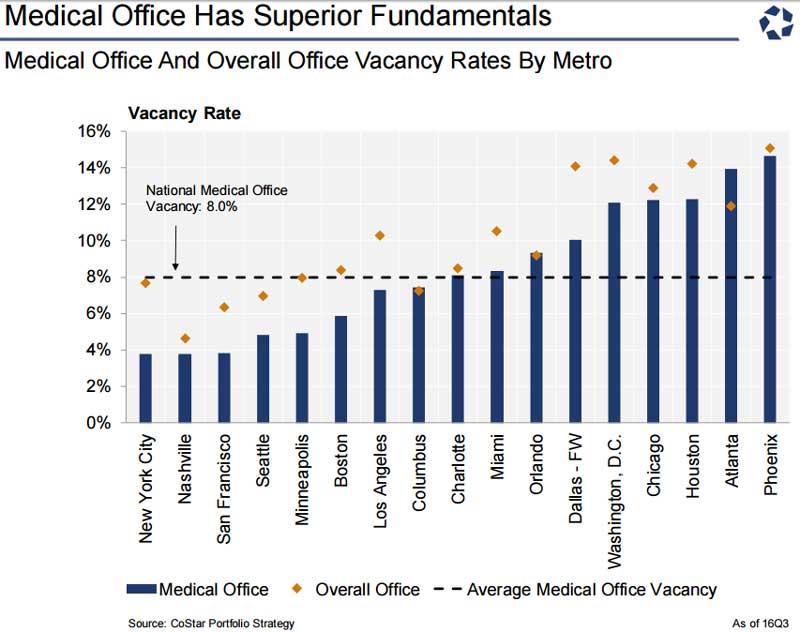

As of the third quarter of 2016, medical-office buildings (MOBs) continued to outperform the broader U.S. office market, achieving over 50% higher demand growth, according to CoStar Portfolio Strategy. The average U.S. medical office vacancy rate of roughly 8% is well about the overall office vacancy rate in all but a few high-construction metros such as San Francisco and Nashville, according to CoStar data.

Along with other income-property types, MOB sales and pricing have slowed in comparison to 2015’s historic peaks. However, MOBs, along with seniors housing, skilled-nursing facilities (SNFs) and hospital properties, continue to attract debt and equity capital, said James Seymour, senior managing director of Capital One Healthcare’s real estate financing team, which closed more than 220 transactions, half of them leveraged loans.

One of those deals was among the largest medical office transactions of the year, In December, the Capital One team served as the lead arranger and book runner for a $535 million loan to mortgage REIT Starwood Property Trust for its acquisition of 34 medical office properties.

CBRE’s U.S. Healthcare Capital Markets Group sold 109 medical facilities in 2016 totaling over 7.2 million square feet, including another of the year’s largest portfolio transactions, the $725 million purchase of 52 medical offices by Physicians Realty Trust, a self-managed health care REIT, from Englewood, CO-based based Catholic Health Initiatives (CHI).

“The market for medical office buildings was particularly robust last year. We saw strong deal flow, driven in part by hospital monetization and consolidation,” Seymour said. “Private buyers took a more active role, as private REITs moved to the sidelines and some public REITs were net sellers of assets for the first time in many years.”

As for health-care REITs, Peter Martin, a health care REIT analyst for JMP Securities, expects year-over-year declines in investment activity during 2017, and flat or slightly depressed capital deployments in 2018. The sector outlook is tempered by a “lack of clarity” regarding health care reimbursement changes under the Trump Administration, Martin said in a preview this week of fourth-quarter 2016 health-care REIT earnings.

Trump Policies Brings Opportunities for Seniors Housing, Challenges for Skilled Nursing

Some skilled nursing and seniors housing operators reported choppy operating performance as regulatory and market changes settle across the post-acute space, Seymour said.

While the long-term outlook for seniors housing remains very strong, operators continue to monitor flattening short-term growth in many metros as the market tries to absorb newly developed assisted-living and memory care properties, and other regulatory and cost pressures.

However, seniors housing stands to be the biggest beneficiary among health-care property sectors from Trump Administration’s policies promoting tax cuts and economic growth, which could lead to deeper demand and stronger investor appetite for seniors housing and more M&A activity this year, JMP’s Martin said.

Preliminary data from Irving Levin Associate indicates the dollar value of publicly announced seniors care M&A transactions was $14.4 billion in 2016, just edging out 2015’s $14.2 billion, though the number of deals declined by 6% to 337 in 2016.

The coming months will be a period of ‘price discovery’ in the skilled-nursing facility and long-term care hospital sectors as fundamentals weaken amid reimbursement concerns and rental rate pressure on SNFs and long-term care hospitals, Martin said. Declining cap rates will also suppress deal volume for quality MOB and senior housing assets, he added.

/wp-content/uploads/2020/08/florida-medical-space-logo.png00ADMIN/wp-content/uploads/2020/08/florida-medical-space-logo.pngADMIN2017-02-13 01:01:132017-02-13 01:01:13Despite Uncertainty Over Drive To Repeal Obamacare, Investors Banking On Demographics To Maintain Healthy Outlook For Health-Care Properties