An affiliate of Acadia Healthcare filed a letter of intent with state officials to establish a new hospital in Miami-Dade County.

The Florida Agency for Health Care Administration received the letter of intent from South Florida Behavioral Health LLC, an affiliate of Franklin, Tennessee-based Acadia Healthcare (Nasdaq: ACHC), for a 104-bed adult inpatient psychiatric hospital. The applicant doesn’t have to specify the location of the hospital within the county until later in the certificate of need application process.

Acadia Healthcare Chief Development Officer Steven T. Davidson, who signed the letter of intent, couldn’t immediately be reached for comment. The company owns 568 facilities that treat addiction and behavioral health problems in 39 states, Puerto Rico and the United Kingdom. Its only South Florida location is the Wellness Resource Center in Boca Raton.

Under the certificate of need process, AHCA determines whether there is sufficient demand for a new hospital and whether the applicant has a suitable plan. Acadia Healthcare’s application is due March 8. The agency would issue its decision on June 2.

/wp-content/uploads/2020/08/florida-medical-space-logo.png00admin/wp-content/uploads/2020/08/florida-medical-space-logo.pngadmin2017-02-27 02:53:402017-02-27 02:53:40Public Company Proposes New Hospital In Miami-Dade

Sen. Jeff Brandes (R-St. Petersburg) filed a bill Wednesday that would open Florida for increased business opportunities in the medical marijuana industry.

Called the Florida Medical Marijuana Act, Brandes’ bill creates a regulatory framework for new entrepreneurs to launch dispensaries.

Under existing law, medical marijuana businesses must function at every aspect of the process from growing and cultivating to dispensing. That means if someone wants to open a dispensary, they must also have a nursery.

Brandes’ bill would change that by allowing a dispensing organization to purchase medical marijuana product at wholesale from a grower, even if that company is a separate entity.

Existing rules are analogous to requiring grocery stores to only sell products they’ve grown, cultivated and packaged themselves. Brandes’ proposal lets companies decide what part of the business they want to tackle.

His bill would limit the number of dispensaries in the state to one per 25,000 residents in each county. That’s still more open than two other proposals looming for Amendment 2 implementation. Another bill filed by Sen. Rob Bradley (R-Orange Park) only allows an additional five businesses six months after the medical marijuana registry reaches 250,000 patients and then five more at various patient benchmarks.

Brandes’ bill protects against critics’ fears that Amendment 2 would lead to “pot shops” on every corner by implementing some limits, but keeps the market open by keeping the maximum high enough for businesses to compete.

Brandes also protects against some other concerns levied by critics, including regulations on where patients can consume marijuana. Based on his bill, patients cannot use the drug in public places, on public transportation, in schools or at work if an employer restricts use.

It also does not exempt patients from legal charges if they are caught driving while under the influence of marijuana.

Entrepreneurs looking to launch in Florida face a $1,000 permit application fee to start a growing, retail or transportation business. Growers would pay up to $50,000 for a license and then again every two years to renew the license. Retail and transport businesses would pay up to $10,000 for a license.

The bill allows local governments to levy a business tax on medical marijuana businesses and gives them the option to ban businesses from their locations. Local governments could also set regulations on location, hours of operation and other business-related details.

Medical marijuana under Brandes’ bill would be subject to sales tax. Revenue would go into a special fund to be used on research and development related to the safety and efficacy of marijuana products.

The bill bans advertising and offers protections against the drug falling into the wrong hands. For example, if someone dies who is registered as a medical marijuana user in the state, that person’s caregiver or personal representative is required to return unused marijuana and the patient’s marijuana ID card to a dispensary.

Under Brandes’ bill, the Florida Department of Health would be required to begin issuing ID cards to patients and their caregivers by Oct. 3. The Department would have 14 days from that date to register the patients in order to issue the ID cards.

The bill eliminates the existing requirement for doctors and patients to have at least a 90-day relationship before the patient can qualify for medical marijuana. The Bradley bill didn’t eliminate that requirement, but did reduce it to 45 days. A Department of Health proposal requires the full 90 days.

The state must establish implementation protocol for Amendment 2, which voters approved in November.

/wp-content/uploads/2020/08/florida-medical-space-logo.png00admin/wp-content/uploads/2020/08/florida-medical-space-logo.pngadmin2017-02-22 19:06:402017-02-22 19:06:40Florida Senator Files Entrepreneurial Medical Marijuana Bill

The new year is already underway and we expect both a new Republican-dominated Congress and President Donald Trump to bring ambitious policy changes to health care. With significant pent up energy among the Republicans and a limited 18-month window for legislation, lawmakers will be in an immediate all-out policy-making mode. This is particularly true for health care, which many in Congress consider a top issue on the docket. With an eagerness for change, health care is in flux, and difficult decisions will need to be made that will directly affect Americans both socially and economically. In this world, many are left wondering what to expect in 2017. Here are the top five health care trends to watch in the New Year.

ObamaCare, Interrupted

In all likelihood, legislation to repeal to the Affordable Care Act (ACA) will be sitting on Trump’s desk in short order. But a replacement plan will be missing and will require the balance of the year or later before it is complete.

Despite all the rhetoric around “repeal and replace,” the governing realities are much more complex. For one, Republicans have a lot of finer points to work out. Five lawmakers and two conservative think tanks have introduced different health care blueprints and Republicans will work to get at least a handful of Democrats to sign onto their proposal, meaning we’re in for a year of consensus building as essential questions are answered and final proposals are built.

For 2017, that may not be too much of an issue. Open enrollment closed on January 31 and those that have ACA coverage will keep it, but the clock is ticking. Insurers will need certainty around the law so they can design plans, set rates and premiums, and decide where they want to participate before some or all of the ACA exchanges phase out. If no replacement is forthcoming, the consequences could be significant, particularly for hospitals and health systems that must provide care regardless of insurance status, with reduced overall payments to offset the expense.

And the pressure is on for lawmakers, as well. Millions of people now depend on the ACA’s benefits — from those who have gained coverage through the marketplaces and Medicaid, to children that can stay on their parents’ plans until age 26, to those receiving no-cost preventive services. A total overhaul could mean taking those benefits away completely, or shifting people into the ranks of the underinsured.

Similar to an elaborate game of Jenga, our health system is made of interconnected pieces that if pulled at the wrong time or the wrong way, may result in the collapse of the entire structure. No question, change is needed. But we also can’t return to the days of millions of uninsured, coverage lock-outs due to pre-existing conditions, emergency rooms as the site of primary care, an unmanaged population that is invisible to the health care system, and ever-escalating costs.

In the end, 2017 will be the year that we move beyond some of the partisan stand offs that have tainted the ACA. One hallmark of these reforms will be moving away from the top-down federal mandate approach toward one that prioritizes customization and state-led innovations.

Health Care Hunger Games

Last year, I wrote about MACRAnomics, or organizational and financial changes to be unleashed with the new physician payment model. The question for 2017 is whether the Republicans will keep expanding current alternative payment models with some necessary improvements, build only on physician-led approaches, or turn the entire movement over to the private sector to figure out on its own.

Each choice has implications, some more advantageous than others. Letting the markets figure it out is in line with Republican ideology about getting government programs out of the way of private sector innovation and consumer choice. And it could be accomplished with Medicare Advantage (MA) plans — a favorite of Republicans because they provide private plans with fixed amount for care, allowing the plans themselves to push providers into alternative payment models (APMs) if that is effective at reducing costs and risk. But to date, such a push has been slow to materialize, with CMS finding that most MA providers remain in fee-for-service (FFS) and focus on cutting rates, not incenting the redesign of care. Moreover, even if MA plans embraced APMs, only about one-third of beneficiaries are covered in these plans, with even lower adoption in some states (2 percent in Wyoming). This means the status quo of FFS payment in Medicare for most providers, which keeps the system tied to volume-based payments that could lead to unsustainable cost growth and budget overruns.

The second option is to alter the current APM through rulemaking to favor physician-led approaches and physician-owned hospitals and outpatient clinics. These approaches could lead to greater employment and consolidation of physicians, as well as a temptation to avoid caring for the highest-risk populations. This in turn would lead to some patients delaying care or turning to emergency rooms for ambulatory treatments.

The last and most advantageous choice is to build on the APMs that are currently in place, with improvements to ensure they work to their full potential. Significant provider sector investments have already been made in these models, and any reversal of the current movement toward value-based care would cost the sector billions. Moreover, they are bearing the predicted fruit. Today, about 30 percent of all Medicare reimbursements are now flowing through an alternative payment model, and just in the Medicare Shared Savings Program, participants have generated $1.29 billion in savings since 2012, while improving quality in 84 percent of all quality indicators. Premier’s experience with our ACO collaborative has actually been even better, delivering three times the return as all the other ACOs in 2015.

Rather than throwing the baby out with the bathwater, I think Republicans will largely keep the current value-based care models in place today, while creating new options that give physicians greater choice. This is the only antidote to perpetual cuts to fee-for-service (which we can most definitely expect in any repeal and replace plan), as well as rising costs for medical devices and drugs. We will see substantive policy changes, such as added use of legal waivers, changes to the measures and benchmarks, fixes to the risk adjustment methodology, and potentially changes to the savings shared back with providers. But no matter how it’s organized, the writing is on the wall — we are long past the days of rewards based on consumption. In 2017, value becomes the new economy and measurement its currency.

50 Shades Of Health Care

While the ACA was predominantly a federal program pushed down to the states, the opposite dynamic is likely to be central to the Republican replacement plan, instead pushing greater control to the states to design their Medicaid programs as they deem fit. This will likely make Medicaid expansion more palatable to conservative Governors and legislatures that previously rejected it, as they will now be given the freedom to structure programs to include personal responsibility requirements such as employment, co-pays, or lifestyle changes. But, to gain the best results, providers need to find more efficient and innovative ways to care for Medicaid recipients. And to make the most of what is likely to be reduced federal financial support, states will need to explore delivery system reforms that improve the health of communities and control costs.

Tapping new advancements in data and enlisting health systems that share the same goal to align their performance to benefit all residents, more providers may push states to pursue Medicaid waivers, particularly those that test delivery system reform. These programs align well with the alternative payment models in MACRA, are budget neutral, and have been shown to align financial incentives with evidence-based best practices in population health management. Using these waivers, states are able to foster a locally driven move away from the fee-for-service mindset that focuses on treating the sick, to a system that emphasizes prevention and wellness — and saves a lot of money in the process.

Take Alabama, which last year won a waiver to provide care to 60 percent of the state’s Medicaid beneficiaries through regional care organizations (RCOs) that receive a set per member, per month fee for all care delivered. Similar to other payment programs, if quality is maintained and the care delivered costs less than what was allotted, the providers keep the remainder. If it costs more, the providers are at risk for the overage. Although Alabama is still working to set this program up, other states, such as Colorado, Maryland, and Washington, with similar experience with these types of waivers have reported strong health care cost and quality gains.

Still other states, such as Ohio and Arkansas, have applied for and won grants to test episode-based bundled payments for certain high-cost acute care episodes, with providers eligible to receiving bonus payments for cost savings if outcome goals are met.

In 2017, I expect many more of these innovative programs to produce results, and states that have been waiting to see the returns will follow with applications modeled on the most successful programs. I also expect that 2017 will be the year that providers increasingly leverage these programs through the creation of provider-sponsored Medicaid managed health plans that contract directly with the state, aligning the financial risk directly with performance across the continuum of care.

Year Of Living Competitively

With this election, many pharmaceutical companies may have thought they would get a reprieve on pricing, but escalating drug costs remains a huge issue on the table.

Drug price increases affect consumers in a number of ways, including insurance premium costs and higher co-pays for therapies. In fact, Blue Cross Blue Shield of Idaho recently increased costs for its plans by 49 percent, attributing 41 percent of the increase to escalating drug costs for beneficiaries. Similarly, in 2016, the top 10 Medicare Part D prescription drug plans increased their premiums by an average of 8 percent, with five of the plans raising premiums by double digits, the highest rate of increase in the program’s history.

Driving some of these price increases are anti-competitive economics. A recent Senate Special Committee on Aging Report found several market dynamics that contribute to the problem, including sole source drugs that allow for monopoly pricing power, small markets that do not provide enough competitive leverage, and closed distribution channels that prevent new competitors from accessing the drug for necessary generic or bioequivalence studies. We expect 2017 to be the year where Congress, the states, and the courts focus less on price controls and more on closing loopholes and market anomalies that have to date worked to prevent competitive forces from modulating prices.

At the regulatory level, we expect bipartisan support for new legislation that would require the Food and Drug Administration (FDA) to fast track new generic drug applications in cases where there are two or fewer manufacturers in the market, levying a decision within 150 days, as opposed to the four plus years it can take today. It’s also safe to assume we’ll see action on efforts to ease closed distribution regulations to allow generics competitors to gain appropriate access to samples that would enable testing of therapeutic equivalence.

In the courts, state, and federal attorneys will take up a myriad of anti-competitive dynamics that have been used for years to extend patents or prevent competition in the marketplace. Suits have already been filed to challenge the biosimilar 180-day waiting period, which today requires biosimilar competitors to notify the brand maker of their intent to market after they have FDA approval, as opposed to in tandem with their filing. This can delay market entry by six months or more. And we can expect more scrutiny of pay-for-delay deals where branded manufacturers reach agreements with generic companies to delay market entry for new products in exchange for cash or other payments of value.

Through The Looking Glass

Consumerism has been on the rise in health care for the better part of a decade, but it hasn’t truly materialized as many would have envisioned. Consumers today have more cost and quality information than ever before, but it can still be difficult to uncover meaningful differences between the various options. In other cases, the information is not personalized to them, providing information on total costs as opposed to their individual out-of-pocket expenses. Moreover, even in cases where consumers have a clear choice, they may not be able to act on it due to health plan or other restrictions.

But as we move into a post-ACA world, we can expect more consumers to become directly exposed to costs through health savings accounts (HSAs) and high-deductibles, meaning that they are going to seek care choices that provide the most value and convenience to them. The net is that providers need to start thinking more broadly in this new world — not just about how they deliver care, but about the total experience. Is the website easy to use and mobile friendly? Can patients book lower cost FaceTime appointments for non-emergency consults? Does the organization provide enough parking? Do patients understand costs up front, before receiving prescribed care? Can you describe your quality in terms that patients can really understand? Is the billing system easy to understand and straightforward?

On the policy front, that could involve some substantial changes, particularly at the state level, where new laws could be enacted to protect or empower consumers that are increasingly becoming the payers for health care services. Already, four states (California, Florida, Connecticut, and Utah) have passed legislation that would cap the amounts that can be collected from “surprise billing” or the practice of billing for out-of-network costs that the individual had no knowledge of receiving. Still more passed laws requiring disclosure of out-of-network costs and billing estimates. And five states (California, Florida, Maryland, Oregon, and New Jersey) have comprehensive sites that allow consumers to compare the prices and charges for common procedures. Going forward, it’s reasonable to assume that there will be greater transparency around cost, quality, and co-pay data to enable consumers to make more informed choices.

Not only is care going beyond the four walls of the provider organization, but so is the entire buying experience. For 2017, clinicians need to stop thinking exclusively about just performing better than their local competitors and start thinking about providing a customer experience that rivals the top consumer brands.

Without question, 2017 is going to be a year of change. But through it all, we must remember the larger purpose. Republican or Democrat, we’re all aligned behind designing a health care system that is coordinated, innovative, cost-effective, high-quality, available, and affordable for all Americans. If we keep the end goals in focus, this could be the year of tremendous promise and progress.

/wp-content/uploads/2020/08/florida-medical-space-logo.png00admin/wp-content/uploads/2020/08/florida-medical-space-logo.pngadmin2017-02-20 00:05:582017-02-20 00:05:58A Look Forward To Health Care In 2017: Top Five Trends

Construction of the $50 million Anderson Family Cancer Institute, a research and cancer treatment center, has started on the grounds of the Jupiter Medical Center.

The 75,000-square-foot institute is the latest project in the rapidly growing non-profit medical center started in 1979 on Military Trail.

The three-floor institute will feature a main atrium with a water feature and two-story fish tank. The first floor will also include a specialty boutique and personal care items for cancer patients. A cafe and a retail pharmacy are also planned.

Recent projects at Jupiter Medical Center include the De George Pediatric Unit in partnership with the Nicklaus Children’s Hospital, the Margaret W. Niedland Breast Center, Anderson Family Orthopedic & Spine Program, the Frank E. and Mary D. Walsh Robotic Surgery Program, and the Florence A. De George Pavilion.

JMC is a not-for-profit 327-bed regional medical center consisting of 207 private acute-care hospital beds and 120 long-term care, sub-acute rehabilitation and Hospice beds. The center has about 1,500 team members, 575 physicians and 640 volunteers.

To date, the JMC Foundation has raised $32 million of the $50 million needed to complete the state-of-the-art facility.

/wp-content/uploads/2020/08/florida-medical-space-logo.png00admin/wp-content/uploads/2020/08/florida-medical-space-logo.pngadmin2017-02-16 15:20:032017-02-16 15:20:03New $50M Cancer Center To Open At Jupiter Medical Center

Health-care REIT stocks definitely caught a cold in the wake of the unexpected November election results. Even as the Dow Jones Industrial Average topped 20,000 for the first time, the health care REIT sector has declined 2.7% over the past three months, with shares of leading companies like HCP, Inc. (NYSE:HCP) tumbling over 10% in the run up and weeks following the election.

To be sure, many market analysts acknowledge health-care markets face many unknowns, chiefly regarding any replacement for the Affordable Care Act (ACA) targeted for repeal by Republicans, and the effects of changes in government reimbursement of medical and seniors housing costs to providers.

According to a new report by the Congressional Budget Office, repealing portions of the ACA, also known as Obamacare, would cause 18 million people to lose their insurance during the first year of a new plan, and lead to 32 million more people becoming uninsured by 2026. Repeal would also lead to a doubling in the prices of premiums paid by those who remain covered in the individual insurance market, according to the CBO.

Not surprisingly, many health-care providers are expected to delay making major commitments until more information about impending changes to the Act becomes available, according to CBRE Group, Inc.’s 2017 Medical Office Building sector outlook.

While any repeal of the ACA without a replacement plan in place could bring a steep drop in health-care visits and demand, CBRE Americas Head of Research Spencer G. Levy, chief economist Jeffrey Havsy and senior managing economist Timothy Savage recently authored a report saying the long-term prospects of heath-care real estate will be affected more by the tens of millions of retiring baby boomers and ongoing health-care industry consolidation and technological advances, than by the vagaries of government health care policy.

“We are certainly in the midst of intense change and corresponding uncertainty in the health care world, particularly when it comes to government reform,” added Matthew Stevens, senior director with The Advisory Board, in a recent conversation with Colliers International Healthcare Services National Director Mary Beth Kuzmanovich. “The true keys to success are less dependent on political particularities. Providing accessible, reliable and affordable health care will remain top priorities,” Stevens said.

CBRE’s analysts also said a full repeal is highly improbable due to the negative impact of millions of Americans immediately losing their insurance and the potential for higher federal deficit spending if the tax revenue underpinning the law is not replaced. But they believe any short-term disruption will be trumped by major population trends.

“Over the long term, the wave of aging baby boomers will drive demand for health care services, irrespective of any regulatory changes,” the report said.

Outlook for MOBs Remains Solid

Health-care REIT stocks definitely caught a cold in the wake of the unexpected November election results. Even as the Dow Jones Industrial Average topped 20,000 for the first time, the health care REIT sector has declined 2.7% over the past three months, with shares of leading companies like HCP, Inc. (NYSE:HCP) tumbling over 10% in the run up and weeks following the election.

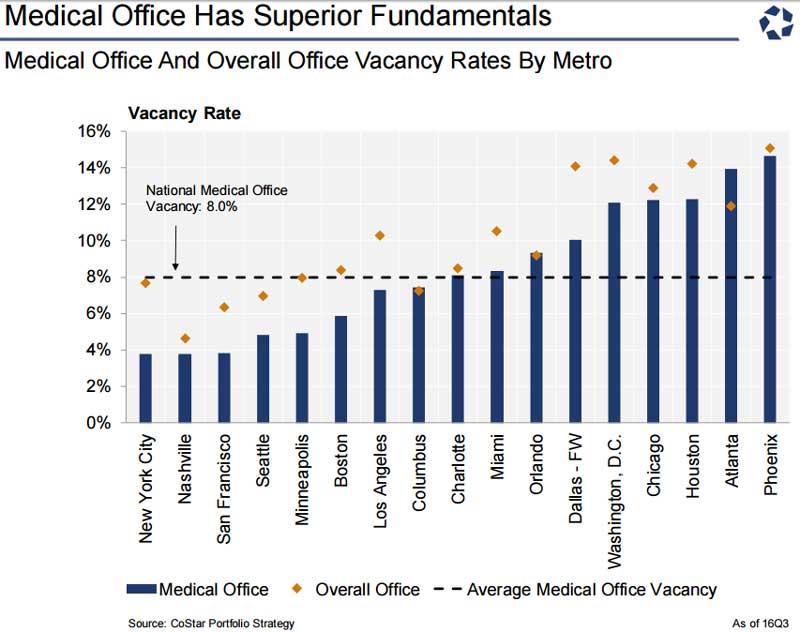

As of the third quarter of 2016, medical-office buildings (MOBs) continued to outperform the broader U.S. office market, achieving over 50% higher demand growth, according to CoStar Portfolio Strategy. The average U.S. medical office vacancy rate of roughly 8% is well about the overall office vacancy rate in all but a few high-construction metros such as San Francisco and Nashville, according to CoStar data.

Along with other income-property types, MOB sales and pricing have slowed in comparison to 2015’s historic peaks. However, MOBs, along with seniors housing, skilled-nursing facilities (SNFs) and hospital properties, continue to attract debt and equity capital, said James Seymour, senior managing director of Capital One Healthcare’s real estate financing team, which closed more than 220 transactions, half of them leveraged loans.

One of those deals was among the largest medical office transactions of the year, In December, the Capital One team served as the lead arranger and book runner for a $535 million loan to mortgage REIT Starwood Property Trust for its acquisition of 34 medical office properties.

CBRE’s U.S. Healthcare Capital Markets Group sold 109 medical facilities in 2016 totaling over 7.2 million square feet, including another of the year’s largest portfolio transactions, the $725 million purchase of 52 medical offices by Physicians Realty Trust, a self-managed health care REIT, from Englewood, CO-based based Catholic Health Initiatives (CHI).

“The market for medical office buildings was particularly robust last year. We saw strong deal flow, driven in part by hospital monetization and consolidation,” Seymour said. “Private buyers took a more active role, as private REITs moved to the sidelines and some public REITs were net sellers of assets for the first time in many years.”

As for health-care REITs, Peter Martin, a health care REIT analyst for JMP Securities, expects year-over-year declines in investment activity during 2017, and flat or slightly depressed capital deployments in 2018. The sector outlook is tempered by a “lack of clarity” regarding health care reimbursement changes under the Trump Administration, Martin said in a preview this week of fourth-quarter 2016 health-care REIT earnings.

Trump Policies Brings Opportunities for Seniors Housing, Challenges for Skilled Nursing

Some skilled nursing and seniors housing operators reported choppy operating performance as regulatory and market changes settle across the post-acute space, Seymour said.

While the long-term outlook for seniors housing remains very strong, operators continue to monitor flattening short-term growth in many metros as the market tries to absorb newly developed assisted-living and memory care properties, and other regulatory and cost pressures.

However, seniors housing stands to be the biggest beneficiary among health-care property sectors from Trump Administration’s policies promoting tax cuts and economic growth, which could lead to deeper demand and stronger investor appetite for seniors housing and more M&A activity this year, JMP’s Martin said.

Preliminary data from Irving Levin Associate indicates the dollar value of publicly announced seniors care M&A transactions was $14.4 billion in 2016, just edging out 2015’s $14.2 billion, though the number of deals declined by 6% to 337 in 2016.

The coming months will be a period of ‘price discovery’ in the skilled-nursing facility and long-term care hospital sectors as fundamentals weaken amid reimbursement concerns and rental rate pressure on SNFs and long-term care hospitals, Martin said. Declining cap rates will also suppress deal volume for quality MOB and senior housing assets, he added.

/wp-content/uploads/2020/08/florida-medical-space-logo.png00admin/wp-content/uploads/2020/08/florida-medical-space-logo.pngadmin2017-02-13 01:01:132017-02-13 01:01:13Despite Uncertainty Over Drive To Repeal Obamacare, Investors Banking On Demographics To Maintain Healthy Outlook For Health-Care Properties